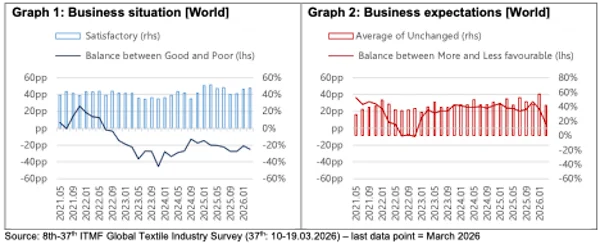

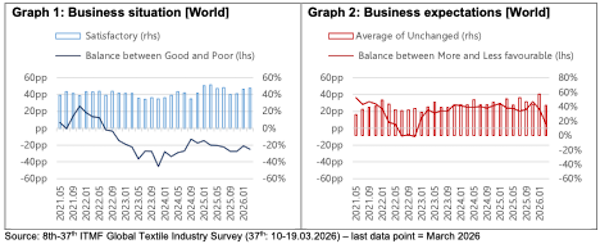

The global textile manufacturing sector is navigating its most precarious period since the 2022 energy crisis, as the International Textile Manufacturers Federation (ITMF) released the results of its 37th Global Textile Industry Survey (GTIS) on April 7, 2026. The findings, gathered during the middle of March 2026, indicate a sharp deterioration in the global business climate, driven primarily by the escalating conflict involving the United States, Israel, and Iran. The survey reveals that for the first time in several years, geopolitical instability has surpassed weak consumer demand as the primary concern for manufacturers, retailers, and machinery producers worldwide. The global business situation balance has plummeted to -25 percentage points, reflecting a industry-wide contraction that has spared few regions or segments.

The Geopolitical Catalyst and Economic Fallout

The primary driver of this sudden downturn is the outbreak of hostilities in the Middle East, which has directly impacted the global energy market and critical maritime trade routes. The 37th GTIS highlights that the "US/Israel-Iran war" has triggered a volatility in energy prices reminiscent of the shocks following the 2022 invasion of Ukraine. As the conflict intensified throughout the first quarter of 2026, the resulting blockade of the Strait of Hormuz—a vital artery for global oil and gas shipments—sent shockwaves through the manufacturing supply chain.

For the textile industry, which is heavily dependent on energy for spinning, weaving, and chemical processing, the surge in fuel and electricity costs has been devastating. Synthetic fiber production, which relies on petroleum-based feedstocks, has seen immediate price hikes, further squeezing the margins of downstream producers. The survey data shows that the global business expectations balance, a key indicator of industry sentiment for the coming six months, collapsed from a relatively healthy +23 percentage points to a meager +5 percentage points. This represents the lowest level of optimism recorded by the ITMF since November 2022, signaling that the industry is bracing for a period of stagflation—a combination of stagnant economic growth and high inflation.

A Chronology of Industry Sentiment and Disruption

The transition from a cautious recovery in late 2025 to the current state of alarm followed a rapid timeline of events. In the fourth quarter of 2025, the 35th and 36th GTIS reports had shown signs of stabilizing demand as global inflation began to cool. However, the geopolitical landscape shifted abruptly in early 2026.

By February 2026, initial skirmishes in the Middle East began to impact shipping insurance rates and fuel surcharges. By the time the ITMF conducted the 37th survey between March 10 and March 19, 2026, the Strait of Hormuz blockade was in full effect. This logistics nightmare forced vessels to take longer, more expensive routes, adding weeks to delivery times for raw materials and finished garments.

The data gathered in March 2026 reflects an industry in "crisis mode." The survey shows that 50% of respondents now cite geopolitics as their top concern, narrowly edging out weak demand (49%). This marks a significant shift from the 36th GTIS, where weak demand was the overwhelming worry for nearly 70% of the industry. Interestingly, the concern over trade tariffs, which had been a dominant theme in 2024 and 2025, dropped from 31% to just 13%, as the immediate physical and financial threats of war overshadowed policy-driven trade barriers.

Regional Divergence: Africa’s Resilience vs. North America’s Decline

The impact of the current crisis is not uniform across the globe, with the 37th GTIS revealing stark regional disparities. Africa emerged as the only region to post a positive business situation balance in March 2026. Analysts attribute this resilience to several factors, including a growing internal market, increased vertical integration in countries like Egypt and Ethiopia, and a lower level of direct exposure to the specific logistics corridors affected by the Hormuz blockade. Furthermore, many African textile hubs have benefited from recent investments in renewable energy, partially shielding them from the global surge in fossil fuel prices.

In contrast, North and Central America recorded the steepest decline in business conditions. The proximity of the United States to the conflict—both diplomatically and militarily—has led to increased domestic market volatility. US-based textile firms and those in Central American "nearshoring" hubs that depend on the US consumer market have seen a sharp contraction in orders as consumer confidence in North America wavers under the threat of a wider war.

South America remains a notable outlier in terms of future outlook. Despite the current global downturn, South American respondents led the world in regional optimism. This is likely due to the region’s relative geographic isolation from the conflict zones and its role as a major producer of natural fibers, such as cotton, which may see increased demand if synthetic production remains hampered by high oil prices. Conversely, South-East Asia has become the most pessimistic region. As a major global export hub for apparel, the combination of soaring freight costs and the threat of stagflation in Western markets has created a "perfect storm" for manufacturers in Vietnam, Cambodia, and Indonesia.

Segment Analysis: Manufacturers vs. Retailers

The 37th GTIS also highlights a widening gap between different segments of the textile value chain. Garment producers have fared the best among all manufacturing segments, largely because they are the closest to the end consumer and have been able to maintain some level of activity through existing backlogs. However, the outlook for the "upstream" segments is significantly more dire.

Textile machinery manufacturers remain in deeply negative territory. This segment is often seen as the "canary in the coal mine" for the industry; when manufacturers stop investing in new equipment, it signals a long-term lack of confidence in capacity expansion. The current negative balance suggests that textile firms are halting capital expenditure (CAPEX) to preserve liquidity in the face of rising operational costs.

Weavers and knitters also reported a deeply negative outlook, caught between the rising costs of yarn and the inability to fully pass those costs on to brands and retailers. Interestingly, brands and retailers themselves remain the most upbeat segment. While their optimism has tempered, they continue to benefit from diverse sourcing strategies and the ability to adjust retail prices more fluidly than a factory can adjust its overhead.

Strategic Responses and Market Diversification

In response to the blockade and the shifting geopolitical alliance, the ITMF survey indicates that firms are intensifying efforts toward market diversification. A significant trend noted in the March 2026 data is an active move away from over-reliance on the US market. Firms are looking toward intra-regional trade and emerging markets in the Global South to mitigate the risks associated with US involvement in the Middle East conflict.

Internal cost absorption has become the primary survival strategy for many manufacturers. With logistics disruptions and raw material costs surging, firms are choosing to trim their own margins rather than risk losing long-term contracts by passing on the full extent of the price increases to their clients. Notably, the survey found that more radical strategies—such as the relocation of production facilities—remain low. This suggests that the industry views the current crisis as a high-intensity, potentially short-to-medium-term disruption rather than a permanent structural shift that would justify the massive capital requirements of moving factories.

Broader Implications and the Risk of Stagflation

The findings of the 37th GTIS serve as a warning for the global economy. The textile industry is often a leading indicator of broader manufacturing health, and the revival of stagflation risks is a concern for policymakers worldwide. The comparison to the 2022 post-Ukraine invasion shock is particularly apt; once again, the global economy is facing a supply-side shock (energy and logistics) at a time when demand was already fragile.

The International Textile Manufacturers Federation, headquartered in Zurich, emphasizes that the recovery of the industry will depend heavily on the duration of the conflict in the Middle East and the stability of the Strait of Hormuz. Should the blockade persist through the second quarter of 2026, the industry may see a wave of consolidations and bankruptcies, particularly among smaller weaving and spinning mills that lack the financial reserves to absorb sustained high energy costs.

As the industry looks toward the ITMF Annual Conference scheduled for later in 2026, the focus will undoubtedly remain on resilience and risk management. The 37th GTIS has made one thing clear: the era of focusing solely on demand and supply-chain efficiency has ended. In 2026, the global textile industry must now master the art of navigating a world where geopolitics dictates the flow of trade as much as the loom or the needle.

For further details on the 37th Global Textile Industry Survey and historical data, the ITMF encourages stakeholders to consult their official resources or contact the secretariat in Zurich. The next survey, expected in May 2026, will be critical in determining whether the industry can find a path to stabilization or if it will sink further into a period of prolonged contraction.