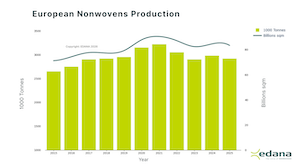

The European nonwovens industry, a critical pillar of the regional textile and manufacturing sector, faced a complex landscape of economic headwinds and shifting consumer behaviors throughout 2025. According to the comprehensive annual statistical report released by EDANA in Brussels on April 7, 2026, the industry recorded a moderate contraction in overall production volume, yet demonstrated a remarkable capacity for structural resilience and technological adaptation. The figures, which cover the "Greater Europe" region—including the European Union, United Kingdom, Turkey, and several neighboring Eastern European nations—indicate that total nonwovens production fell by approximately 2.2% compared to the previous year, settling at a total output of 2,919,000 tonnes.

This slight decline marks a period of stabilization following the volatile fluctuations experienced during the early 2020s, characterized first by the unprecedented demand for personal protective equipment (PPE) during the pandemic and subsequently by the energy price shocks of 2023 and 2024. While the headline figure of a 2.2% drop suggests a cooling market, a deeper analysis of the data reveals a more nuanced picture of an industry in transition, balancing traditional high-volume sectors with emerging specialized applications.

Analyzing the Macroeconomic Drivers of 2025

The 2025 performance of the nonwovens sector was dictated by several converging macroeconomic factors. High interest rates throughout much of the year continued to dampen the construction and automotive sectors, both of which are significant consumers of nonwoven materials. Furthermore, the European manufacturing base faced intensified competition from overseas producers, particularly from Asian markets, where lower energy costs and labor expenses allowed for more aggressive pricing on commodity-grade roll goods.

Jacques Prigneaux, EDANA’s Market Analysis and Economic Affairs Director, provided context for these figures, noting that the industry has had to navigate a "perfect storm" of reduced domestic demand in certain segments and a challenging global trade environment. "Despite the negative impact of several drivers affecting the nonwovens industry, the slowdown in demand across some key market segments, and an increasing competition from abroad, the European nonwovens industry has once again demonstrated its strength, resilience, flexibility, and ability to innovate," Prigneaux stated.

A Chronology of Industry Performance: 2020–2025

To understand the 2025 figures, it is essential to view them within the historical trajectory of the last five years. The nonwovens industry has undergone a significant "boom-and-bust" cycle that has now transitioned into a "new normal."

- 2020–2021: The industry saw record-breaking growth, particularly in meltblown and spunbond technologies, as manufacturers pivoted to meet the global demand for face masks, medical gowns, and disinfectant wipes.

- 2022–2023: A period of correction followed as stockpiles of PPE were depleted and consumer spending shifted from goods to services. This period was also defined by the European energy crisis, which forced many producers to implement surcharges or temporarily halt production lines.

- 2024: The industry showed signs of recovery with a 1.7% growth in the hygiene sector, signaling a return to pre-pandemic consumption patterns.

- 2025: The current reporting year reflects a consolidation phase. The 2.2% decline is viewed by analysts not as a sign of industry failure, but as a recalibration toward sustainable long-term output levels in the face of demographic shifts and environmental regulations.

Technological Divergence: Spunmelt vs. Specialized Processes

The EDANA report highlights a significant divergence in performance across different production technologies. Not all segments of the industry felt the contraction equally, suggesting that manufacturers focusing on specialized high-value processes fared better than those in high-volume commodity markets.

Spunmelt Technologies: The spunmelt sector, which includes spunbond and meltblown processes used heavily in hygiene and medical applications, saw the most significant decline at 3.3%. This was largely attributed to the saturation of the hygiene market and the increased penetration of imported goods. As the largest technological segment by volume, the contraction in spunmelt had a disproportionate impact on the overall industry tonnage.

Drylaid and Short-Fiber Technologies: Drylaid production remained relatively stable, recording a marginal decline of only 0.7%. This stability is often attributed to the versatility of drylaid nonwovens, which find applications in everything from filtration to home furnishings.

Growth in Specialized Bonding: Interestingly, certain segments bucked the downward trend. Hydroentanglement (spunlace) recorded a modest growth of 0.1%. This process is essential for the production of wipes, a market that has remained robust despite broader economic cooling. Even more notable was the 0.8% growth in needle-punched bonding processes. Needle-punched nonwovens are frequently used in geotextiles, filtration, and infrastructure projects, suggesting that government-funded civil engineering projects across Europe provided a crucial safety net for producers in this niche.

Market Segment Breakdown: Hygiene, Wipes, and Industrial Uses

The hygiene market remains the cornerstone of the European nonwovens industry, accounting for the largest share of total volume. However, in 2025, this segment declined by 2.7%. This contraction was primarily driven by the baby diaper market. Demographic trends across Europe, characterized by declining birth rates in several major economies, have led to a shrinking domestic market for traditional hygiene products. Additionally, the rise of "eco-conscious" consumerism has led to a preference for thinner, more efficient materials, which reduces the total tonnage required even if the number of units sold remains steady.

In contrast, the personal care wipes segment saw a 0.9% increase in roll goods sales. This growth reflects the continued integration of convenience-based cleaning products into daily European life. However, this sector faces looming regulatory challenges as the European Union’s Single-Use Plastics (SUP) Directive continues to influence material composition, pushing manufacturers toward more expensive cellulosic and biodegradable fibers.

The industrial sectors showed more volatility:

- Building and Roofing: This segment saw a sharp decline of 6.8%. High borrowing costs in 2024 and early 2025 stalled many residential and commercial construction projects, reducing the demand for roofing membranes and insulation underlays.

- Automotive Interiors: Production for the automotive sector fell by a slight 0.9%. While the transition to electric vehicles (EVs) provides new opportunities for nonwovens in battery insulation and sound dampening, the overall stagnation in European car manufacturing volumes limited growth.

- Upholstery and Home Furnishings: This sector experienced the steepest decline at 7.1%, reflecting a broader pull-back in discretionary consumer spending on durable goods.

The "Grammage" Factor and Hidden Value

An important caveat noted by EDANA is that tonnage figures alone do not tell the full story of industry health. The report mentions that these statistics do not account for specific "grammage" developments—the weight per square meter of the material. In recent years, there has been a significant trend toward "lightweighting"—producing thinner, stronger, and more efficient nonwovens.

For many manufacturers, a decrease in tonnage does not necessarily mean a decrease in square meters produced or in total revenue. By producing lighter materials, companies can reduce raw material costs and improve the sustainability profile of their products. EDANA provides detailed surface area data to its members, which often reveals a more positive growth trajectory than weight-based statistics suggest.

Industry Reactions and the Path to Sustainability

The release of the 2025 statistics has prompted a call for continued innovation within the European supply chain. Industry observers note that the slight decline in production volume is an incentive for European firms to double down on high-tech, sustainable solutions that cannot be easily replicated by low-cost competitors.

Environmental sustainability has moved from a peripheral concern to a core business strategy. The 2025 data reflects an industry in the midst of a "green transition." Producers are increasingly incorporating recycled polymers and natural fibers such as flax, hemp, and wood pulp into their nonwoven webs. This shift is partly a response to the EU Green Deal and the Circular Economy Action Plan, which mandate higher rates of recyclability and reduced carbon footprints for manufactured goods.

"The direct input from producers, combined with a comprehensive monitoring of the industry, results in a valuable business tool for our member companies," Prigneaux added, emphasizing that the data serves as a roadmap for future investment in R&D.

Looking Ahead: INDEX™ 26 in Geneva

The full scope of the 2025 data and the projected trends for 2026 and 2027 will be the primary focus of the upcoming INDEX™ 26 exhibition. Scheduled to take place in Geneva, Switzerland, in May 2026, INDEX™ is the world’s leading nonwovens exhibition, bringing together thousands of professionals from across the global supply chain.

EDANA has announced that more detailed figures, categorized by specific production processes and micro-market segments, will be disclosed during the event. A "Market Trends Seminar" is scheduled for Tuesday, May 19, 2026, at 2:00 p.m., where Prigneaux and other industry experts will provide a deep dive into the 2025 statistics and offer a forecast for the remainder of the decade.

The seminar is expected to address critical questions regarding the future of the European nonwovens industry, including how to navigate the aging demographic of the hygiene market and how to capitalize on the growing demand for filtration media in the face of stricter air and water quality regulations.

Conclusion: A Strategic Pivot

The 2025 statistics released by EDANA underscore a period of strategic pivot for the European nonwovens industry. While a 2.2% decline in production volume reflects the immediate pressures of global competition and economic cooling, the growth in specialized sectors like needle-punching and personal care wipes points toward a resilient and adaptable manufacturing base.

As the industry moves toward INDEX™ 26, the focus remains on innovation, sustainability, and the move toward high-value applications. By leveraging its technological expertise and commitment to quality, the European nonwovens sector appears well-positioned to maintain its global leadership, even as the landscape of manufacturing continues to evolve in a post-pandemic, carbon-conscious world.