While consumer brands have long borne the brunt of scrutiny regarding their sustainability practices, a significant power player in the retail ecosystem has largely operated outside the spotlight: the landlords behind shopping centers, high streets, and retail precincts. This oversight is rapidly changing, signaled prominently by the recent launch of the Sustainable Retail Index Association (SRIA). This new initiative marks a pivotal moment, shifting the focus towards the environmental, social, and governance (ESG) responsibilities of those who curate the physical spaces where the majority of global retail transactions still occur.

The retail landlord sector, comprising companies that own and manage vast portfolios of commercial real estate, wields immense, often unseen, influence over the retail landscape. These entities dictate the brand mix within their properties, shape the physical shopping experience, and can profoundly impact the operational decisions of their tenant brands. From the design and energy efficiency of buildings to waste management systems and the types of services offered, landlords possess a unique leverage point to drive sustainable transformation across the entire retail value chain. Yet, historically, the industry and consumers alike have primarily directed their ESG demands toward the brands manufacturing and selling goods, overlooking the foundational role of the spaces in which these transactions take place.

An Overlooked Powerhouse in the Sustainability Equation

The traditional narrative of retail sustainability has centered on product life cycles, ethical supply chains, and consumer purchasing choices. Brands have faced escalating pressure from activists, regulators, and increasingly conscious consumers to demonstrate their commitment to environmental protection, fair labor practices, and transparent governance. However, the physical infrastructure that houses these brands—the malls, plazas, and standalone stores—has, until now, remained a blind spot in comprehensive sustainability assessments. This is a critical omission, given that landlords control the infrastructure, utilities, and often the operational guidelines for hundreds, if not thousands, of tenant businesses. Their decisions can influence everything from a store’s energy consumption to its waste generation and the availability of circularity services like repair or recycling.

The sheer scale of their operations underscores this influence. Major retail landlords manage millions of square feet of commercial space, housing diverse portfolios of tenants ranging from global fashion giants to independent local businesses. By selecting which brands occupy their spaces, they directly shape the consumption ecosystem accessible to millions of shoppers daily. They can, therefore, act as gatekeepers, nudging the industry towards more "responsible" consumption by prioritizing tenants with strong ESG credentials or by implementing property-wide initiatives that support sustainable practices.

The Genesis of the Sustainable Retail Index Association

The launch of the Sustainable Retail Index Association (SRIA) represents a concrete step to address this "missing link" in retail sustainability. Announced recently, the SRIA is co-founded by two of the world’s largest retail landlords: Unibail-Rodamco-Westfield (URW), a global leader in commercial real estate, and Ingka Centres, the parent group of IKEA, which operates meeting places around the world. This collaboration signals a significant commitment from key industry players to collectively tackle sustainability challenges at a portfolio level.

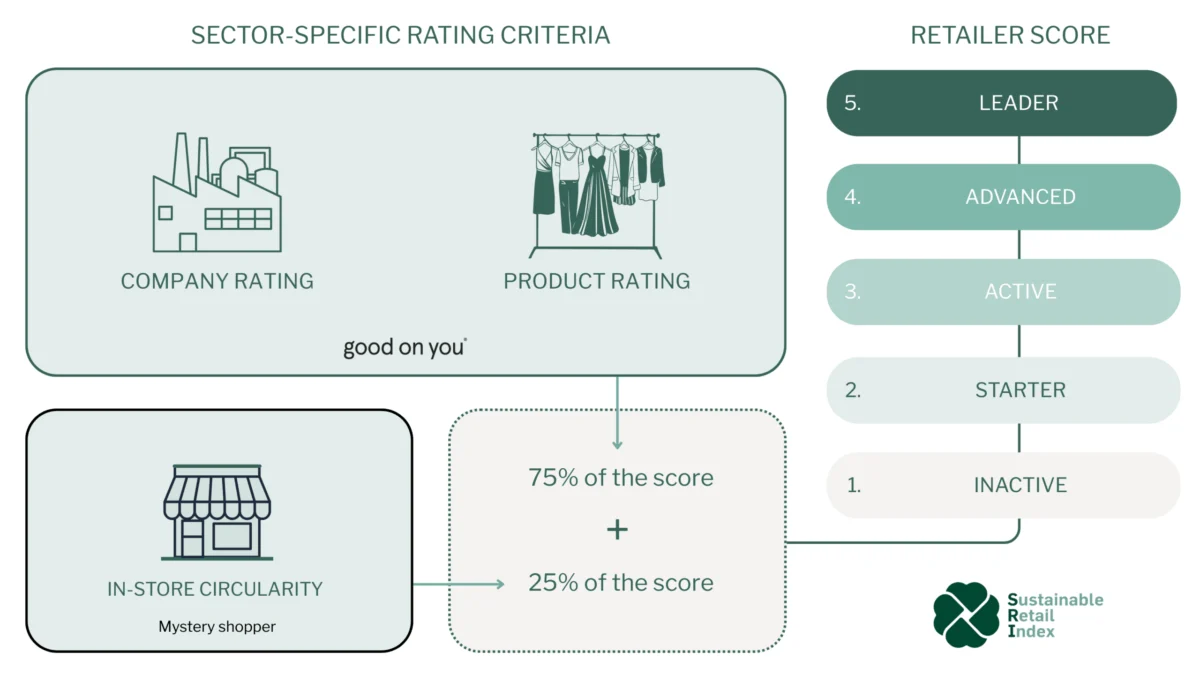

The primary objective of the SRIA is to establish a standardized framework for measuring the sustainability performance of tenant portfolios. This is a crucial development because, prior to this, landlords lacked a consistent, universally accepted method to evaluate the ESG impact of the diverse array of brands operating within their properties. The Association aims to provide landlords with actionable data, enabling them to identify sustainability hotspots, track progress, and foster improvements across their entire tenant base.

Good On You, a leading platform for ethical brand ratings, serves as the data partner behind the SRIA. Their expertise in assessing fashion brands’ impact on people, the planet, and animals is integral to the Index’s methodology. Sandra Capponi, co-founder of Good On You, highlighted the rigorous approach taken to ensure the Index is based on reliable, transparent, and publicly available information. The development of the Index itself was a collaborative effort, with Good On You initially partnering with URW to create this assessment tool, which the new Association now seeks to establish as an industry-wide standard.

The Index operates by combining Good On You’s established brand rating data with assessments of in-store practices. This holistic approach evaluates not only a brand’s broader value chain sustainability but also its specific actions within the physical retail space, such as the provision of circularity services like repairs, rentals, or recycling points. This granular data is increasingly sought after by landlords who wish to gain a deeper understanding of their tenants’ impact and proactively address ESG issues at both the individual store and overall shopping center level.

Driving Forces: Why Now is the Time for Landlord Accountability

The emergence of initiatives like the SRIA is not an isolated event but rather a response to a confluence of powerful forces reshaping the business landscape.

1. Escalating Consumer Demand for Ethical Choices: While online shopping has seen exponential growth over the past decade, physical retail remains the dominant shopping channel globally. In 2024, approximately 73% of UK retail sales occurred in physical stores. In the US, while e-commerce sales are projected to reach $1.6 trillion by 2028, this will still only constitute about 24% of total retail sales, according to Forrester research. This underscores the enduring importance of physical spaces.

Consumers, particularly younger generations, are increasingly vocal about their desire for sustainable products and ethical brands. Research consistently shows a significant "attitude-behavior gap," where shoppers express a strong intent to buy sustainably but often struggle to translate this into actual purchases. Barriers include difficulty identifying sustainable options, lack of awareness of where to find them, and general confusion about what "sustainability" truly entails. Landlords, by curating a more sustainable tenant mix and integrating circular services, can directly address these barriers, making it easier for consumers to make informed and responsible choices. Sandra Capponi emphasizes this point: "People don’t want to be in places that are just promoting the same old fast fashion; they want variety and options to make better decisions. And if landlords want to drive foot traffic for their retailers, they need to create a better, more diverse offering."

2. The Imperative of ESG-Focused Investing: A primary driver behind landlords’ increasing focus on sustainability is the relentless pressure from ESG-focused investors. According to Morgan Stanley research, a striking 88% of global investors are interested in companies that deliver both financial and ESG-linked returns. Despite some political backlash against ESG in certain regions, institutional investors, particularly in Europe, continue to pose rigorous questions about climate risk, supply chain ethics, and social impact.

Retail landlords managing multi-billion-dollar real estate portfolios are increasingly being asked to demonstrate how they are de-risking their assets against climate change impacts, how they are ensuring ethical practices among their tenants, and how they are contributing positively to the communities they serve. Comprehensive, portfolio-level sustainability data, such as that provided by the SRIA, allows landlords to tell a compelling story to investors, proving their proactive approach to managing ESG risks and capitalizing on sustainability opportunities. This translates directly into commercial incentives, influencing access to capital, cost of financing, and ultimately, asset valuation.

3. Evolving Regulatory Landscape: While not explicitly detailed in the original article, the broader regulatory environment is undeniably contributing to this shift. Governments globally are introducing stricter regulations on corporate sustainability reporting, supply chain due diligence, and environmental impact. The European Union’s Corporate Sustainability Reporting Directive (CSRD) and the proposed Corporate Sustainability Due Diligence Directive (CSDDD), for instance, will significantly expand the scope and depth of sustainability reporting requirements for large companies, including many retail landlords and their tenants. Proactive measures like the SRIA allow landlords to prepare for, and even influence, these evolving regulatory demands.

Reimagining Retail: From Consumption Hubs to Circularity Centres

The shift in focus to landlords’ roles is catalyzing a broader reimagining of physical retail spaces themselves. The aspiration is to transform these venues from mere "shrines to consumerism" into dynamic "hubs of education and circularity." This involves a wide array of initiatives, both in partnership with retailers and independently, aimed at integrating sustainable practices into the core experience of shopping.

Anna Drozdowski, Global Head of Sustainable Retail and Social Impact for URW, articulates this vision: "We are convinced that there is a role to play for landlords to engage with retailers. It’s about how we can support tenants on ESG diagnosis and improvement with dedicated tools." Beyond the Sustainable Retail Index itself, landlords are implementing practical changes within their properties. These "in-store upgrades" can range from basic improvements like the removal of single-use plastic bags and the introduction of refill stations for beauty or cleaning products, to more fundamental changes in infrastructure such as ensuring efficient waste and recycling systems and implementing energy-efficient lighting across common areas and individual stores.

URW, for example, is actively integrating circularity into its centers by collaborating with tenants to introduce rental, resale, and repair services. A notable example is their partnership with Sojo, a next-generation alterations platform, which has launched in Westfield centers in London and Paris. Sojo offers an omni-channel repair service, combining online booking with on-site drop-off and collection points. Drozdowski explains the rationale: "The intention behind it was to ask, how can we play our role to support retailers in offering services that maybe they can’t do themselves for different reasons?" This highlights landlords’ potential to provide shared infrastructure and services that individual tenants might find challenging to implement alone, thereby democratizing access to circular economy solutions.

Beyond large-scale landlords, multi-brand retailers are also pioneering this reimagining. Percy Langley, a UK-based retailer stocking only British brands, exemplifies how physical retail spaces can become multi-purpose community hubs. Founder Poppy Sherbrooke describes their stores as "event spaces" that foster engagement beyond mere transactions. They host repair workshops led by designers, showcasing visible mending techniques, and organize upcycling workshops where textile waste is transformed into new products, such as Christmas decorations. These initiatives not only educate consumers but also create opportunities for community connection and engagement with the design process, even for those not looking to purchase new items. This approach directly tackles the "attitude-behavior gap" by making sustainable practices accessible, tangible, and desirable.

The Clear Business Case for Proactive Action

The momentum behind the SRIA and similar initiatives is firmly rooted in a compelling business case. Landlords like URW and Ingka Centres are not merely pursuing sustainability as a moral obligation; they recognize the tangible commercial benefits. As Sandra Capponi states, "It’s not just a moral obligation; it’s commercial too. At many levels, there’s an appetite for shopping centres to do more."

The business case unfolds across several dimensions:

- Risk Management: By understanding the sustainability performance of their tenant portfolios, landlords can better manage risks associated with supply chain ethics, environmental compliance, and evolving consumer expectations. This proactive approach can mitigate reputational damage and potential financial liabilities.

- Enhanced Customer Experience and Foot Traffic: A curated tenant mix that prioritizes sustainable brands and offers circular services appeals directly to the growing segment of conscious consumers. Providing "better options" and making it easier to shop responsibly can drive increased foot traffic, enhance customer loyalty, and differentiate properties in a competitive retail market.

- Stakeholder Engagement: Demonstrating a commitment to sustainability allows landlords to effectively engage with a broad spectrum of stakeholders, including investors, regulators, local communities, and potential tenants. This strengthens their brand reputation and facilitates smoother operations.

- Competitive Advantage: In an increasingly crowded and evolving retail landscape, sustainability can become a key differentiator. Landlords who can offer genuinely sustainable retail environments and tenant mixes will be better positioned to attract desirable brands and secure long-term leases.

- Attracting Capital: As highlighted earlier, the interest of ESG-focused investors is a powerful financial incentive. Landlords capable of demonstrating robust portfolio-level sustainability data and clear strategies for improvement will be more attractive to capital, potentially securing more favorable financing terms and higher valuations.

The "power of scale" possessed by major retail landlords offers an unprecedented opportunity for systemic change. As Poppy Sherbrooke notes, "The scale that these businesses are working at gives them so much scope and power to make significant change very quickly." Their ability to influence hundreds or thousands of tenants simultaneously, coupled with their control over vast physical infrastructure, means their sustainability initiatives can have a ripple effect across the entire retail ecosystem.

Future Outlook and Challenges

The launch of the Sustainable Retail Index Association marks a promising start, but its ultimate impact will hinge on sustained momentum and genuine, measurable accountability. The goal is for the SRIA to evolve into an industry standard, enabling consistent benchmarking and driving continuous improvement. This could eventually empower retail landlords to integrate ESG criteria directly into their leasing strategies, curating brand mixes not just for demographic fit but also for sustainability performance.

However, challenges remain. The complexity of data collection across diverse tenant portfolios, ensuring tenant buy-in and accurate reporting, and guarding against potential greenwashing are critical hurdles. The industry must ensure that these initiatives translate into tangible environmental and social benefits, moving beyond mere "marketing opportunities" to foster profound operational and cultural shifts.

As retail landlords embrace their pivotal role in driving sustainability, the industry conversation is irrevocably shifting. By treating sustainability as a core portfolio-level concern, rather than an auxiliary marketing effort, they are poised to transform physical retail spaces into powerful catalysts for more responsible consumption and a more circular economy. The potential for significant change is immense, and the early signals suggest a determined trajectory towards a more sustainable retail future.